What is Fixed Deposit?

Fixed deposit (FD) is a financial instrument where a sum of money given to a bank, financial institution or company whereby the receiving entity pays interest at a specified percentage for the time duration of the deposit. The rate of interest paid for fixed deposit vary according to amount, period and from bank to bank. At the end of the time period of the deposit the amount that is originally given is returned to the investor.

Fixed deposit can be opened for a minimum period of 7 days to maximum of 10 years.

All Resident individuals (Including Minors) and HUF are eligible to open a fixed deposit account

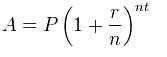

Compound interest arises when interest is added to the principal so that from that moment on, the interest that has been added also itself earns interest. This addition of interest to the principal is called compounding.

The following formula gives you the total amount one will get if compounding is done:-

In this case there is no compounding effect because the term is only one year, the same as the compounding frequency. Thus, all we have is simple interest (i. e. , the effective rate is equal to the nominal rate)

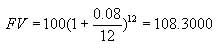

In this case there are 12 compounding periods. Interest earned each month is added to the balance and is itself available to earn interest in each succeeding month. Thus, the future value is greater than the amount calculated using annual compounding.

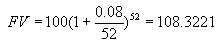

increases the impact of the interest rate. That it does so should be intuitive: more interest is available sooner to earn more interest. Whereas before we had to wait until the end of the month before the interest was ‘added back to the pot’, now it is being credited each week.

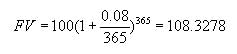

Now instead of earning interest weekly, we earn it daily. As expected the, the impact of the interest rate is magnified. However, this time the impact is not as dramatic as might be expected.

Interest that is, hypothetically, computed and added to the balance of an account every instant. This is not actually possible, but continuous compounding is well-defined nevertheless as the upper bound of “regular” compound interest. The result is the maximum effect that compounding frequency can exert on a given interest rate and term.

All Resident individuals (Including Minors) and HUF are eligible to open a fixed deposit account

Premature withdrawal or Breaking a fixed deposit means withdrawing the money before the maturity expires. This may be necessary if you urgently require the funds or if there are better investment opportunities elsewhere. Many people want to close their old Fixed Deposit account before maturity and open a new account when they see the current interest rates on fixed deposits in the market much higher than rate of interest at which they have opened FD sometime back.

Most of the banks charge premature withdrawal penalty in the form of a 0. 5-1% lower interest on customers looking to close their Fixed Deposit

In the event of the FD being closed before completing the original term of the deposit, interest will be paid at the rate applicable on the date of deposit, for the period for which the deposit has remained with the Bank, with premature closure penalty.

The Bank on request from the depositor, will allow withdrawal of term deposit before completion of the period of the deposit as per terms agreed upon at the time of placing the deposit.For such premature withdrawals and partial withdrawals, the Bank will levy a penalty of 1%, on the applicable rate.Partial withdrawal is permitted in units of Rs 1,000. The balance amount earns the original rate of interest.

In order to access funds at a short interval, one can avail a loan against fixed deposits held with the bank. It is given in the form of an overdraft against your deposited amount. This is an alternative given to customer by bank instead of breaking the deposit prematurely.

Loan against fixed deposit is a great option for those looking to avail a loan at a better rate when compared to personal loans where interest rates range from 14-30% p.a. Moreover, you will continue to earn interest on the deposit though you have availed a loan against it.

Most of the banks allow a loan in the range of 70-90% of the deposit amount. Some banks even offer more than this range. There is no standard on the amount of loan that can be sanctioned. It varies from bank to bank and also upon the amount deposited.

Interest rate charged on the loan given on a fixed deposit is usually 2-2.5% above the interest paid by the bank on the deposit. Once again, it varies from bank to bank.

Traditionally, Fixed Deposits (FD) have been seen as a secure and profitable medium of investment. However, many people, especially investors in the higher tax brackets, ignore a crucial detail when it comes to Fixed Deposits- the interest earned through FD is taxable in line with an individual’s tax slab. Consequently, this detail ensures that your returns from FD investments is actually lower than expected. For example- If you are in the 30% income tax slab and have a fixed deposit that gives you 9% interest, the actual interest passed down to you after the tax cuts is just 6%. Thus, having a working knowledge of how taxes work in terms of an FD helps you stay on top of things.

Remember that interest on fixed deposits are calculated annually or on a cumulative basis. However, the same FD is taxed on an accrual basis, meaning revenue is recognized when earned and expenses are recognized when incurred. Thus, the timeline on reception of the interest on your FD isn’t a factor for tax to be imposed upon it. You will have to pay the corresponding tax at the end of the financial year, and even in situations when the interest isn’t taxable, it must be displayed on your IT returns.

Tax-saver FDs are popular instruments for saving on taxes.

The amount invested in these FDs qualify for deductions U/S 80C of the Income Tax Act,1961.

Money invested in these FDs is locked-in for at least 5 years. This is the minimum time-requirement to qualify for the deduction. Premature withdrawal is not allowed. If the deposit is encashed before maturity, the amounts held under this scheme do not qualify for deductions.

The maximum amount allowed as deduction is Rs.1.5 lakhs. This is as per changes in the law, effected as of Nov.13, 2014. (Under the Bank Term Deposit Scheme, 2006 this amount was limited to Rs.1 lakh). The minimum deposit amount is Rs.100.

Only the principal invested can be claimed as deduction U/S 80C. Interest earned under this scheme is taxable. TDS is charged @10% on the interest earned during a financial year and thereafter according to the deposit-holders applicable tax-bracket.

Interest rates are determined by the bank offering this product. They are usually in line with other deposits of similar tenures. Interest earned can either be paid-out or reinvested/compounded.

Non-Resident Ordinary (NRO) Rupee Accounts are maintained by non-resident Indians (NRI) in Indian Rupees, to keep funds that belonged to them before they turned NRI. These accounts can also be used to account for fresh earnings in Indian Rupees even after the individual has turned an NRI, from such sources as house rent, dividend and interests, salary etc. The interest earned from such accounts is taxable as per the Indian income tax regulations. Currently, Indian banks offer an interest rate from 8-10% on fixed accounts that fulfil the NRO parameters.

Alternatively, a Non-Resident External (NRE) Rupee Accounts are maintained by non-resident Indians (NRI) in Indian Rupees and are meant for foreign exchange that is earned in their country of residence and then transferred to India. The interest earned from such accounts is tax free and the funds can be moved around to other accounts without any restrictions. Currently, Indian banks offer an interest rate from 7-10% on fixed accounts that fulfil the NRE parameters.

In order to improve credit scores, or manage credit more responsibly, banks offer secured credit cards i.e. credit cards issued against a fixed deposit (FD) held with the issuing bank.

Credit cards are usually not given to risky customers i.e. those who are not creditworthy. e.g. those who have poor credit scores, bad histories of managing debt, poor track records of paying dues, defaults on payments etc..

In case of payment defaults: Banks can make recoveries from the fixed deposit if dues are not cleared on secured cards. Regular credit cards are unsecured and unpaid dues can either be written off or recovered through legal recourse.

Debit cards require the cardholder to maintain adequate funds in his/her account prior to using the card. Secured Credit Cards allow cardholders can make spends, payment for which will be fulfilled at a later date.